Yesterday, the GOP officially released its replacement plan for the Affordable Care Act, although leaked details of the plan have been trickling out since last week. In a nutshell, here’s how the replacement plan, formally known as the new “American Health Care Act,” works:

- Eliminates both the individual mandate and the employer mandate.

- Retains the ACA’s popular pre-existing conditions requirement, but allows insurers to charge higher premiums to consumers who allow their coverage to lapse.

- Medicaid-expansion states (as well as states that haven’t yet expanded) would still be able to enroll people (and would still receive ACA funding levels) in the expanded program until 2020, at which point new enrollment would freeze. Also beginning in 2020, the bill replaces Medicaid’s current open-ended federal funding system with a capped, per-capita federal payment to states.

- Eliminates the ACA’s cost-sharing subsidies for low-income Americans and replaces the ACA’s tax credits with credits that do not rise with income (although, in the latest version of the bill, high-income people will not be eligible for the credits). The credits range in value from $2,000 per year (for younger people), to $4,000 per year (for older folks).

While the plan has not yet been officially scored by the Congressional Budget Office, a number of researchers have already analyzed the likely effects of the plan. By and large, poor people will get less assistance under the American Health Care Act than they do under the ACA, while wealthier Americans will benefit from both premium subsidies they wouldn’t have been eligible for under the ACA; the ultra-rich, meanwhile, will pay lower taxes.

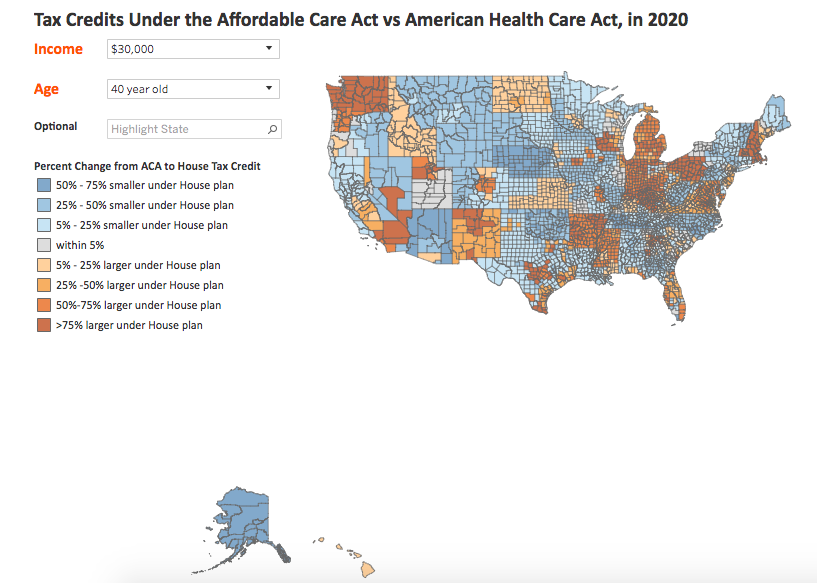

The Kaiser Family Foundation unveiled an interactive graphic this morning that compares ACA and AHCA tax credits for consumers in different states, at different income levels. “Generally, people who are older, lower-income, or live in high-premium areas (like Alaska and Arizona) receive larger tax credits under the ACA than they would under the American Health Care Act replacement,” the KFF researchers wrote. “Conversely, some people who are younger, higher-income, or live in low-premium areas (like Massachusetts, New Hampshire, and Washington) may receive larger assistance under the replacement plan.”

Earlier today, over at Vox, a group of health-care economists led by David Cutler, one of the architects of the ACA, released an analysis of the new GOP plan. “We estimate that the bill would increase costs for the average enrollee by $1,542, for the year, if the bill were in effect today,” Cutler and his colleagues concluded. “In 2020, the bill would increase costs for the average enrollee by $2,409.”

The replacement plan would be particularly tough on older Americans (those aged 55 to 64), who would see their costs “increase by $5,269 if the bill went into effect today and by $6,971 in 2020.” Low-income Americans (those earning under 250 percent of the poverty line) “would see their costs increase by $2,945 today and by $4,061 in 2020.” Cutler and his colleagues also predict that the AHCA’s changes would also lead to a sicker risk pool, driving up premiums.

Criticism hasn’t been limited to the liberal side of the aisle. Conservative health-care wonk Avik Roy, whose ACA replacement plan seems to be the only conservative plan that actually increases insurance coverage rates, is not a fan. In an op-ed published in Forbes today, Roy writes that the proposed credits will “price many poor and vulnerable people” out of the market and predicts that the CBO “is likely to score the AHCA as covering around 20 million fewer Americans than Obamacare.”

“Expanding subsidies for high earners, and cutting health coverage off from the working poor: it sounds like a left-wing caricature of mustache-twirling, top-hatted Republican fat cats,” Roy concludes. “But not today.”

It’s unclear if the GOP has enough votes to pass this kind of replacement plan. A number of ultra-conservative conservatives have expressed doubts that the plan is too generous, while a group of moderate Republican senators have announced they will not support a plan that doesn’t protect enrollees in the expanded Medicaid program.