Should the GOP repeal Obamacare and fail to pass a replacement, some 59 million Americans could find themselves uninsured.

By Dwyer Gunn

(Photo: Luke Sharrett/Getty Images)

Earlier this week, Senate Republicans announced their embrace of the so-called “Repeal and Delay” strategy, which calls for an immediate repeal of the Affordable Care Act but defers the effective date of the repeal for several years in order to allow the GOP to work out the specifics of a replacement plan.

The strategy isn’t popular among hospitals, insurers, or health-care experts (including those who aren’t Obamacare fans). Perhaps for good reason. A new report from the Health Policy Center at the Urban Institute, a think tank, lays out the many dangers of the strategy.

Here’s what the report, co-authored by Linda Blumberg, Matthew Buettgens, and John Holahan, assumes the repeal would change:

Since only components of the law with federal budget implications can be changed through reconciliation, this approach would permit elimination of the Medicaid expansion, the federal financial assistance for Marketplace coverage (premium tax credits and cost-sharing reductions), and the individual and employer mandates; it would leave the insurance market reforms (including the nongroup market’s guaranteed issue, prohibition on preexisting condition exclusions, modified community rating, essential health benefit requirements, and actuarial value standards) in place.

Repeal and Delay would likely have immediate effects on the individual insurance marketplace. The disappearance of the individual and employer mandates could send the non-group market, which is already fragile, into a tailspin. Without a mandate, some participants (particularly the healthy ones) will drop their coverage and stop paying their premiums, resulting in a sicker risk pool. And insurers, many of whom are already losing money in these markets, may simply decide to pull out of the exchanges in the face of market uncertainty and expectations of declining enrollment and a sicker risk pool.

All in, the report concludes that, “if the individual and employer mandates are eliminated while the ACA’s Medicaid expansion, Marketplace tax credits and cost-sharing reductions, insurance market reforms, and other components are left in place in 2017, 4.3 million people would drop their ACA-compliant non-group insurance coverage and become uninsured (table 8).” And if the repeal eliminates premium and cost-sharing subsidies, the effects will be larger.

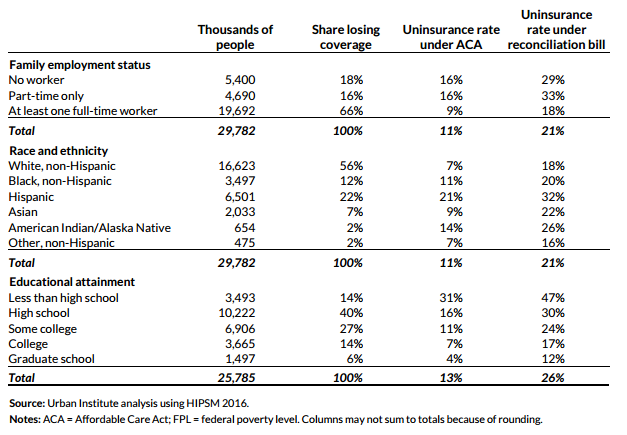

The report also takes a look at what would happen if the GOP repeals the Affordable Care Act and fails to pass a replacement in time—a scenario that, though unlikely, is certainly not outside the realm of possibility. The numbers here are particularly grim: The Urban Institute estimates that the population of uninsured people in the United States would increase by 29.8 million people, or 103 percent, to 58.7 million. Twenty-one percent of non-elderly adults would lack health insurance.

(Chart: Health Policy Center)

The affected population would be disproportionately white, and lacking a college degree, as the chart to the left (from the report) illustrates. “This scenario does not just move the country back to the situation before the ACA,” the report’s authors write. “It moves the country to a situation with higher uninsurance rates than was the case before the ACA’s reforms.”

These numbers, of course, are a worst-case scenario. The political consequences of failing to pass a replacement for the ACA are dire, and the GOP is no doubt well aware of that fact. There are also steps the GOP could take to stabilize the individual insurance market during the planning period, such as keeping subsidies in place, or reactivating the risk management programs. Republican staffers are reportedly studying such options, as well they should; doing nothing would be catastrophic.